-

Investment

Start SIP Invest Monthly

SIF Investment Build wealth with Specialised Funds

Freedom SIP Plan Your Future with Freedom SIP

Start Lumpsum Invest One Time

Index Fund Readymade Index Portfolios

International Fund Buy Foreign Companies

New Fund Offer Invest in Newly Launched Funds

Gold Fund Buy 24k Digital Gold

- Explore

-

Tools

SIP Calculator Calculate Future value of SIP Investment

SWP Calculator Plan Your Wealth with Our SWP Calculator

Step-Up SIP Calculator Step Up Your SIP Strategy with Our Calculator

STP Calculator Calculate Your STP Returns Easily

MF Portfolio OverlapCheck Common Stocks Before You Invest

Compare Funds Detailed comparison of funds in

MF Screener Pinpoint the right funds

Client Assessment Know your investment personality

All Calculator All Financial Calculators at your Fingertips

-

Blogs

Mutual Fund Research Reports Detail Analysis of Mutual Fund

MF Expert Views Views by Expert on News

Mutual Fund News Find Latest News & Updates

Mutual Fund Learning Learn Concept of Mutual Funds

Newsletter Read market update month wise

Web Story Quick informative & trending stories

Blogs Explore trends, tips & strategies

-

NEW

Pro Services

NEW

NEW

Retirement Planning Grow your wealth for a comfortable retirement

Expert Curated Portfolios Smart portfolios crafted by market specialists

Funds Recommendations Get best funds shortlisted by expert for 2026

Portfolio Check-up Fix your portfolio with top MF Analyst

Personalised SIP Portfolio Get portfolio customised according to your needs

Loan Against Mutual Funds Get instant cash against securities

Debt Mutual Funds

- Total Funds 433

- Average annual returns 10.27%

What is Debt Mutual Funds?

The debt mutual funds refer to investment vehicles that pool money from different investors to invest in a diversified asset or portfolio. Debt mutual funds aim to offer stable returns with lower risk than equities and government bonds, corporate bonds and treasury bills are the ideal option.

- Steady income from interest on debt instruments

- High liquidity, allowing investors to redeem their money anytime

- Ideal for conservative investors or for looking for short-to medium-term goals.

Top Performing Debt Funds in India for High Returns

Returns

SIP Returns

Risk

Information

NAV Details

Data in this table : Get historical returns. If 1Y column is 10% that means, fund has given 10% returns in last 1 year.

Select date points :

Submit| Fund Name | AUM (Cr.) | Fund Age | 1W | 1M | 3M | 6M | YTD | 1Y | 2Y | 3Y | 5Y | 10Y | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 87.95 | 11 years | 0.06% | 0.45% | 6.76% | 8.42% | 13.79% | 16.87% | 11.34% | 9.59% | 27.31% | 2.29% | Invest | |

| 1390.96 | 11 years | 0.06% | 1.07% | 2.21% | 4.48% | 7.89% | 11.93% | 14.34% | 12.12% | 9.95% | 8.47% | Invest | |

| 10.97 | 17 years | -0.05% | 0.79% | 2.98% | 5.1% | - | 10.03% | 9% | 8.73% | 7.8% | - | ||

| 257.78 | 23 years | 0.09% | 1.27% | 1.73% | 7.95% | 7.87% | 9.99% | 16.28% | 15.96% | 12.35% | 8.07% | Invest | |

| 97.20 | 18 years | 0.2% | 0.77% | 2.22% | 4.38% | - | 8.88% | 8.67% | 7.9% | - | - | ||

| 52.99 | - | 0.71% | 1.25% | 2.14% | 4.18% | - | 8.64% | 7.51% | 6.36% | 5.83% | 6.73% | ||

| 52.99 | - | 0.71% | 1.24% | 2.14% | 4.18% | - | 8.64% | 7.51% | 6.35% | 5.83% | 6.81% | ||

| 3127.29 | 17 years | 0.05% | 1.01% | 2.19% | 3.84% | 5.45% | 8.51% | 11.14% | 9.87% | 12.05% | 8.51% | Invest | |

| 6212.04 | 15 years | 0.1% | 0.97% | 2.08% | 3.73% | 3.9% | 7.85% | 8.64% | 8.4% | 7.31% | 7.8% | Invest | |

| 353.88 | 12 years | 0.03% | 0.96% | 2.29% | 4.17% | 4.09% | 7.64% | 8.35% | 7.97% | 6.86% | 6.72% | Invest | |

| - | 12 years | 0.14% | 0.54% | 1.77% | 3.68% | - | 7.51% | 7.12% | 7.24% | 7.81% | - | ||

| 2174.86 | 22 years | 0.06% | 1.09% | 2.37% | 4.5% | 4.37% | 7.06% | 7.96% | 7.79% | 7.04% | 7.18% | Invest | |

| 5492.19 | 21 years | 0.06% | 1.07% | 2.15% | 3.62% | 3.61% | 7% | 8.23% | 7.83% | 6.82% | 7.34% | Invest | |

| 1486.26 | 21 years | 0.07% | 0.62% | 1.95% | 4.01% | 3.94% | 7% | 8.41% | 8.14% | 7.19% | 5.92% | Invest | |

| 767.90 | 16 years | 0.14% | 1.06% | 1.95% | 3.28% | 3.42% | 6.88% | 7.4% | 7.61% | 5.84% | 6.56% | Invest | |

| 12.80 | 18 years | 0.11% | 0.44% | 1.52% | 3.12% | - | 6.87% | 6.77% | 6.26% | 5.19% | 5.96% | Invest | |

| 160.47 | 11 years | 0.07% | 0.78% | 3.15% | 4.46% | 4.49% | 6.77% | 8.53% | 8.45% | 7.22% | 5.64% | Invest | |

| 2737.06 | 1 years | 0.09% | 0.62% | 1.69% | 3.66% | 3.74% | 6.75% | - | - | - | - | Invest | |

| 7522.50 | 12 years | 0.09% | 0.93% | 2.03% | 3.87% | 3.78% | 6.68% | 7.78% | 7.58% | 6.56% | 7.39% | Invest | |

| 8.59 | 17 years | 0.11% | 0.45% | 1.53% | 3.1% | - | 6.64% | 6.76% | 6.26% | 4.88% | 5.92% | Invest |

| Fund Name | AUM (Cr.) | Risk | 1W | 1M | 3M | 6M | YTD | 1Y | 2Y | 3Y | 5Y | 10Y |

|---|

| Fund Name | Jul-2026 | Jun-2026 | May-2026 | Apr-2026 | Mar-2026 | Feb-2026 | Jan-2026 | Dec-2025 | Nov-2025 | Oct-2025 | Sep-2025 | Aug-2025 |

|---|

| Fund Name | 2026-Q3 | 2026-Q2 | 2026-Q1 | 2025-Q4 | 2025-Q3 | 2025-Q2 | 2025-Q1 | 2024-Q4 | 2024-Q3 | 2024-Q2 | 2024-Q1 | 2023-Q4 |

|---|

| Fund Name | 2026 | 2025 | 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 |

|---|

| Fund Name | AUM (Cr.) | Risk | 1W | 1M | 3M | 6M | YTD | 1Y | 2Y | 3Y | 5Y | 10Y |

|---|

| Fund Name | AUM (Cr.) | Initial NAV | Final NAV | NAV Change | Absolute Ret. | Annalized Ret. |

|---|

| Fund Name | AUM (Cr.) | Risk | 6M | 1Y | 2Y | 3Y | 5Y | 10Y | From Launch | |

|---|---|---|---|---|---|---|---|---|---|---|

| 87.95 | Very High |

4.79%

|

21.47%

|

15.24%

|

12.36%

|

17.08%

|

10.41%

|

8.62%

|

Invest | |

| 1390.96 | Moderate |

2.63%

|

12.38%

|

13.41%

|

13.42%

|

11.76%

|

9.35%

|

9.14%

|

Invest | |

| 10.97 | Moderate |

-

|

-

|

-

|

-

|

-

|

-

|

1.71%

|

||

| 257.78 | High |

5.84%

|

15.33%

|

15.55%

|

15.55%

|

14.41%

|

10.16%

|

8.29%

|

Invest | |

| 97.20 |

-

|

-

|

-

|

-

|

-

|

-

|

1.18%

|

|||

| 52.99 | Low to Moderate |

-

|

-

|

0.44%

|

2.2%

|

3.4%

|

4.38%

|

5.11%

|

||

| 52.99 | Low to Moderate |

-

|

-

|

0.44%

|

2.2%

|

3.4%

|

4.39%

|

4.75%

|

||

| 3127.29 | High |

2.46%

|

9.43%

|

10.19%

|

10.54%

|

11.17%

|

9.77%

|

9.18%

|

Invest | |

| 6212.04 | Very Low |

2.31%

|

8.19%

|

8.47%

|

8.57%

|

8.12%

|

7.79%

|

8.03%

|

Invest | |

| 353.88 | Low |

2.49%

|

8.46%

|

8.35%

|

8.33%

|

7.76%

|

6.96%

|

6.97%

|

Invest | |

|

-

|

-

|

-

|

-

|

-

|

1.22%

|

3.26%

|

||||

| 2174.86 | Low |

2.65%

|

8.51%

|

8.06%

|

8.06%

|

7.78%

|

7.25%

|

7.76%

|

Invest | |

| 5492.19 | Very Low |

2.44%

|

7.92%

|

8.03%

|

8.15%

|

7.7%

|

7.35%

|

7.67%

|

Invest | |

| 1486.26 | Moderate |

2.14%

|

7.66%

|

8.11%

|

8.27%

|

7.92%

|

6.56%

|

6.76%

|

Invest | |

| 767.90 | Moderate |

2%

|

7%

|

7.5%

|

7.59%

|

6.98%

|

6.38%

|

7.01%

|

Invest | |

| 12.80 | Low |

-

|

-

|

1.1%

|

2.46%

|

3.67%

|

4.21%

|

5.72%

|

Invest | |

| 160.47 | Moderate |

2.83%

|

8.74%

|

8.38%

|

8.46%

|

8.35%

|

6.4%

|

6.27%

|

Invest | |

| 2737.06 | Average |

1.91%

|

7.16%

|

-

|

-

|

-

|

-

|

7.04%

|

Invest | |

| 7522.50 | Low |

2.25%

|

7.56%

|

7.51%

|

7.7%

|

7.32%

|

7.29%

|

7.46%

|

Invest | |

| 8.59 | Low |

-

|

-

|

1.1%

|

2.43%

|

3.66%

|

4.19%

|

5.6%

|

Invest |

| Fund Name | Risk | Standard Deviation | Alpha | Beta | Sharpe Ratio | |

|---|---|---|---|---|---|---|

| Very High |

4.11%

|

3.31%

|

-

|

0.73%

|

Invest | |

| Moderate |

2.99%

|

4.87%

|

0.29%

|

1.76%

|

Invest | |

| Moderate |

-

|

-

|

-

|

-

|

||

| High |

7.39%

|

9.44%

|

-

|

1.22%

|

Invest | |

|

-

|

-

|

-

|

-

|

|||

| Low to Moderate |

1.44%

|

-

|

0.42%

|

-

|

||

| Low to Moderate |

1.44%

|

-

|

0.42%

|

-

|

||

| High |

2.04%

|

2.65%

|

0.70%

|

1.59%

|

Invest | |

| Very Low |

1.17%

|

1.64%

|

0.14%

|

1.56%

|

Invest | |

| Low |

1.13%

|

1.33%

|

0.09%

|

1.27%

|

Invest | |

|

-

|

-

|

-

|

-

|

|||

| Low |

1.09%

|

1.22%

|

0.05%

|

1.16%

|

Invest | |

| Very Low |

1.43%

|

0.65%

|

0.79%

|

0.95%

|

Invest | |

| Moderate |

1.01%

|

1.51%

|

0.10%

|

1.61%

|

Invest | |

| Moderate |

1.56%

|

0.83%

|

0.20%

|

0.73%

|

Invest | |

| Low |

0.391%

|

-

|

-

|

-

|

Invest | |

| Moderate |

1.94%

|

2.00%

|

-

|

1.01%

|

Invest | |

| Average |

-

|

-

|

-

|

-

|

Invest | |

| Low |

1.23%

|

0.90%

|

0.13%

|

0.89%

|

Invest | |

| Low |

0.357%

|

-

|

-

|

-

|

Invest |

| Fund Name | Min SIP | Min Lumpsum | Expense Ratio | Fund Manager | Launch Date | |

|---|---|---|---|---|---|---|

|

₹1000

|

₹5000

|

1.38%

|

Alok Singh

|

27-Feb 2015

|

Invest | |

|

₹1000

|

₹100

|

1.36%

|

Sunaina Da Cunha

|

17-Apr 2015

|

Invest | |

|

₹0

|

₹5000

|

0.6%

|

-

|

12-Dec 2008

|

||

|

₹100

|

₹100

|

1.01%

|

Vivek Ramakrishnan

|

13-May 2003

|

Invest | |

|

₹0

|

₹5000

|

0.1%

|

-

|

16-Jul 2008

|

||

|

₹500

|

₹1000

|

0.83%

|

Ruchi Fozdar

|

18-Mar 2013

|

||

|

₹500

|

₹1000

|

0.83%

|

Ruchi Fozdar

|

24-Nov 2014

|

||

|

₹1000

|

₹1000

|

1.32%

|

Sunaina Da Cunha

|

25-Mar 2009

|

Invest | |

|

₹100

|

₹100

|

1.17%

|

Manish Banthia

|

03-Dec 2010

|

Invest | |

|

₹1000

|

₹5000

|

1.57%

|

Devang Shah

|

15-Jul 2014

|

Invest | |

|

₹0

|

₹1000

|

-

|

-

|

04-Mar 2014

|

||

|

₹500

|

₹5000

|

1.55%

|

Lokesh Mallya

|

16-Jul 2004

|

Invest | |

|

₹1000

|

₹5000

|

1.18%

|

Manish Banthia

|

15-Sep 2004

|

Invest | |

|

₹100

|

₹500

|

1.26%

|

Kinjal Desai

|

08-Jun 2005

|

Invest | |

|

₹100

|

₹100

|

1.72%

|

Deepak Agrawal

|

11-May 2010

|

Invest | |

|

₹200000

|

₹10000

|

0.13%

|

-

|

09-Oct 2007

|

Invest | |

|

₹1000

|

₹1000

|

1.24%

|

Vikas Garg

|

04-Sep 2014

|

Invest | |

|

₹100

|

₹100

|

0.26%

|

Anupam Joshi

|

12-May 2025

|

Invest | |

|

₹100

|

₹100

|

1.51%

|

Dhruv Muchhal

|

25-Mar 2014

|

Invest | |

|

₹200000

|

₹10000

|

0.15%

|

-

|

05-Sep 2008

|

Invest |

| Fund Name | Current NAV | Previous NAV | 1D NAV Change | 52- Week High NAV | 52- Week Low NAV | |

|---|---|---|---|---|---|---|

|

14.3001

(16-07-2026)

|

14.2966

(15-07-2026)

|

0.02%

|

14.301

|

12.2396

|

Invest | |

|

25.1758

(16-07-2026)

|

25.1518

(15-07-2026)

|

0.1%

|

25.2166

|

22.5289

|

Invest | |

|

()

|

()

|

0%

|

-

|

-

|

||

|

54.8304

(16-07-2026)

|

54.7822

(15-07-2026)

|

0.09%

|

54.8916

|

49.8478

|

Invest | |

|

()

|

()

|

0%

|

-

|

-

|

||

|

40.0725

(27-01-2025)

|

()

|

0.31%

|

-

|

-

|

||

|

40.4031

(27-01-2025)

|

()

|

0.31%

|

-

|

-

|

||

|

43.5415

(16-07-2026)

|

43.5016

(15-07-2026)

|

0.09%

|

43.6279

|

40.1745

|

Invest | |

|

34.5027

(16-07-2026)

|

34.4642

(15-07-2026)

|

0.11%

|

34.5315

|

32.0357

|

Invest | |

|

23.1810

(16-07-2026)

|

23.1663

(15-07-2026)

|

0.06%

|

23.2143

|

21.5533

|

Invest | |

|

()

|

()

|

0%

|

-

|

-

|

||

|

49.1779

(16-07-2026)

|

49.1186

(15-07-2026)

|

0.12%

|

49.2457

|

45.9595

|

Invest | |

|

48.2799

(16-07-2026)

|

48.2274

(15-07-2026)

|

0.11%

|

48.384

|

45.1287

|

Invest | |

|

37.7566

(16-07-2026)

|

37.7347

(15-07-2026)

|

0.06%

|

37.7953

|

35.3242

|

Invest | |

|

31.6598

(16-07-2026)

|

31.6184

(15-07-2026)

|

0.13%

|

31.6739

|

29.6682

|

Invest | |

|

33.3055

(25-03-2025)

|

33.3003

(24-03-2025)

|

0.02%

|

-

|

-

|

Invest | |

|

2072.605

(16-07-2026)

|

2070.4911

(15-07-2026)

|

0.1%

|

2074.39

|

1940.24

|

Invest | |

|

10.8308

(16-07-2026)

|

10.827

(15-07-2026)

|

0.04%

|

10.8308

|

10.1495

|

Invest | |

|

25.8124

(16-07-2026)

|

25.781

(15-07-2026)

|

0.12%

|

25.8357

|

24.2278

|

Invest | |

|

30.4741

(25-03-2025)

|

30.4692

(24-03-2025)

|

0.02%

|

-

|

-

|

Invest |

Debt Funds Return Calculator

Historical Returns

Future Value

Invested Amt.

+Net Profit

=Total Wealth

- Invested Amount

- Estimated Returns

- Invested Amount ₹43,855

- Interest Earned ₹6,145

Explore Other Popular Calculators

Types of Debt Mutual Funds

![]() All

All

![]() Park Your Savings

Park Your Savings

![]() Better than FDs

Better than FDs

![]() Debt for Long Term

Debt for Long Term

![]() Others

Others

HSBC Focused Fund - Regular Growth

3Y Returns 15.23 % (p.a.)

VS

HSBC Focused Fund - Regular Growth

3Y Returns 15.23 % (p.a.)

VS

Kotak Focused Fund- Regular plan _ Growth Option

3Y Returns 15.23 % (p.a.)

Kotak Focused Fund- Regular plan _ Growth Option

3Y Returns 15.23 % (p.a.)

Nippon India Nifty 50 Value 20 Index Fund - Regular Plan - Growth Option

3Y Returns 15.23 % (p.a.)

VS

Nippon India Nifty 50 Value 20 Index Fund - Regular Plan - Growth Option

3Y Returns 15.23 % (p.a.)

VS

Motilal Oswal Nifty Smallcap 250 Index - Regular Plan

3Y Returns 15.23 % (p.a.)

Motilal Oswal Nifty Smallcap 250 Index - Regular Plan

3Y Returns 15.23 % (p.a.)

Tata Money Market Fund-Regular Plan - Growth Option

3Y Returns 15.23 % (p.a.)

VS

Kotak Money Market Fund - (Growth)

3Y Returns 15.23 % (p.a.)

Tata Large & Mid Cap Fund- Regular Plan - Growth Option

3Y Returns 15.23 % (p.a.)

VS

Tata Money Market Fund-Regular Plan - Growth Option

3Y Returns 15.23 % (p.a.)

VS

Kotak Money Market Fund - (Growth)

3Y Returns 15.23 % (p.a.)

Tata Large & Mid Cap Fund- Regular Plan - Growth Option

3Y Returns 15.23 % (p.a.)

VS

ICICI Prudential Large & Mid Cap Fund - Growth

3Y Returns 15.23 % (p.a.)

ICICI Prudential Large & Mid Cap Fund - Growth

3Y Returns 15.23 % (p.a.)

How Do Debt Mutual Funds Work?

The debt mutual funds function by investing in a range of different portfolios of fixed-income assets.This is how it works:

- Diversify Portfolio: Spreads across investments across different debt instruments, reducing the risks associated with individual bonds.

- Professional Management: Expert fund managers make the investment decisions based on market conditions and the fund’s objectives.

- Risk & Returns: Offers a predictable income stream in the form of dividends. The interest rates and credit quality of the underlying securities influence the return.

- Liquidity: Provides investors with high liquidity, and they can buy or sell units in Debt funds quickly.

Types of Debt Mutual Funds

Here are the different types of best debt mutual funds, including investment goals and risk factors:

Short-Term Debt Funds

Invests in debt securities having maturities from 1 to 3 years. Thus, it offers moderate returns with lower interest rate risk.

- Liquid Fund

- Money Market Fund

- Overnight Fund

- Ultra-short Duration Fund

- Low Duration Fund

- Short Duration Fund

- Floater Fund

Medium-Term Debt Funds

Medium-term debt funds are mainly suitable for investors seeking a balance between risk and return. It includes bonds and securities having maturities of 3-5 years.

- Medium Duration

- Medium to Long Duration Fund

Long-Term Debt Funds

Long-term debt funds offer higher returns, but they are sensitive to interest rate changes. The ideal length of investment duration is a minimum of 5 years or more.

- Long-duration fund

- A dynamic bond fund

Corporate & Institutional debt Funds

Majorly invests in corporate bonds and debentures. Its rerun largely depends on the credit quality and interest rates of issuing companies.

- Corporate bond fund

- Banking and PSU

- Credit risk fund

Government & Market-Based Debt Funds

Institutional debt funds usually include money market instruments and government securities, and are often considered low risk and have a predictable return.

- Gilt Fund

Advantages of Investing in Debt Mutual Funds

The best Debt mutual funds provide a stable, low-risk way to earn regular income, while preserving capital and maintaining better liquidity.

Below are some advantages of investing in debt mutual funds:

- Professional Management & Return: Gives access to money markets and wholesale debt markets, providing retail investors the chance to earn interest and capital gains on debt managed by professionals.

- Multiple Investment Options: Investorscan choose a wide range of maturities that match their risk tolerance. Short-term funds extend consistent income, while longer-duration funds are suited for those comfortable with higher NAV volatility.

- Lower Risk Compared to Equities:Debt funds are appropriate for short-term objectives and offer steady returns. Those who are looking for fewer risks than equity funds are a good option as they offer good debt mutual funds returns in future.

- High Liquidity: Unlike fixed deposits, there is no lock-in period, it offers speedy redemption, usually within one or two working days.

Pro tips: With the help of SIP Calculator you can calculate the best return in future.

Risks of Debt Mutual Funds

These mutual funds fundamentally carry three different types of risks involved:

- Credit Risk: This is the default risk of the issuer not repaying the interest and principal amount.

- Interest Rate Risk: Is the effect of changing interest rates on the value of the scheme’s securities.

- Liquidity Risk: This is the risk carried by the fund house of not having adequate liquidity to meet redemption requests

Debt Mutual Funds Returns: What to Expect?

The debt mutual funds offer stable, low-risk returns that often outperform savings accounts and fixed deposits, making them perfect for short-to medium-term goals with maintaining liquidity and flexibility:

Key points to consider:

- Historical Performance: Short-duration and liquid funds largely deliver 4-7% annulaized returns. On the other hand, long-duration and gilt funds can offer higher returns but are more sensitive to interest rate changes.

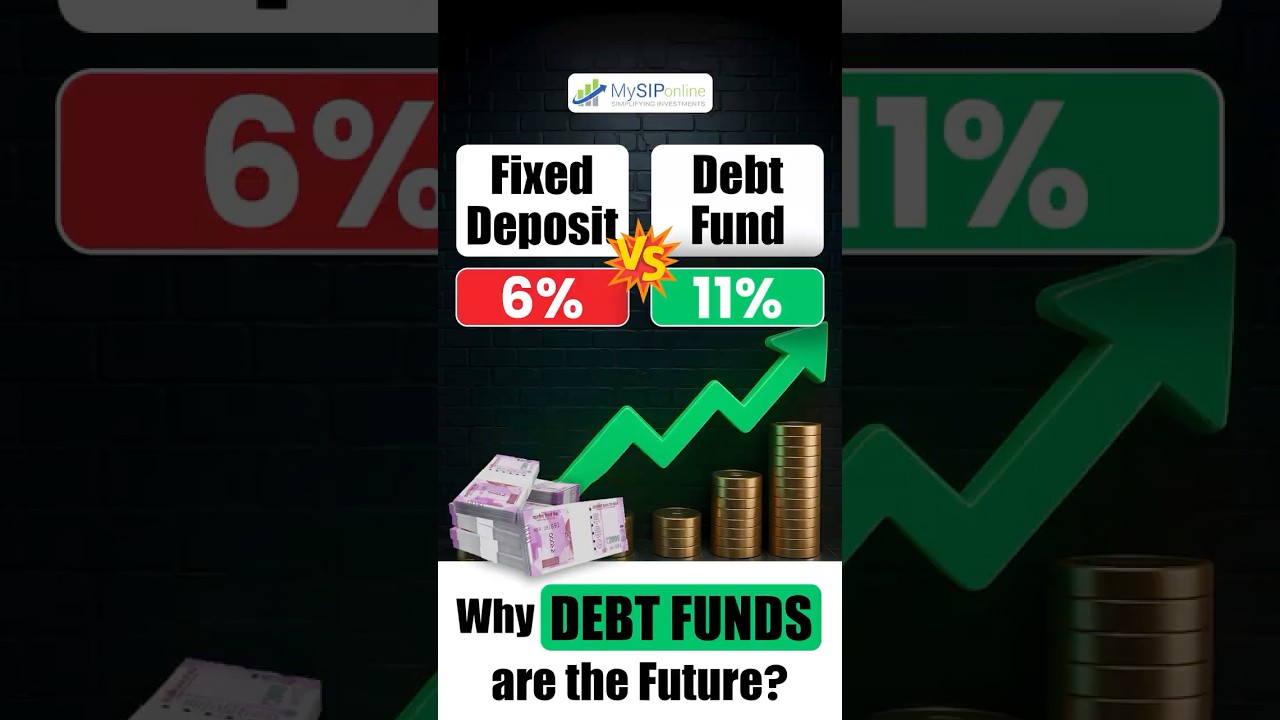

- Comparison with FDs & Savings Accounts: Debt funds usually offer better post-tax returns and liquidity than traditional fixed deposits and savings accounts.

- Factors Affecting Returns: Interest rate movements, credit quality and fund management strategies all influence performance.

Best Debt Mutual Funds to Invest In 2026

You can plan finances confidently with the best debt mutual funds to invest in 2026, delivering steady, risk-managed growth.

Aditya Birla SL Medium Term

This is the medium-duration debt fund that mainly invests in corporate bonds and possibly in other fixed-income securities with a maturity of 3 to 5 years. The purpose is to deliver relatively stable returns with moderate interest rate risk.

Important details are as follows:

- Fund Type: Medium Duration Debt Fund

- Investment Horizon: 3-5 years

- Risk Involved: Moderate

- Portfolio Focus: Corporate bonds and debt securities

- Perfect for: Investors seeking stable income with minimum/moderate risk

SBI Magnum Gilt-G

This gilt fund that primarily invests in government securities, generally issued by the government of India. It carries no credit risk but may fluctuate based on interest rate movements.

Key Details:

- Fund Type: Gilt Fund

- Investment Horizon: Medium to long term

- Risk Involved: Moderate, as the interest rate is sensitive

- Portfolio Focus: Government securities

- Ideal for: High-quality sovereign debt investments

DSP Gilt-G

DSP guilt fund focuses on investing in long-term government securities, giving high credit safety. The performance of the fund is largely influenced by changes in interest rates.

Key Details:

- Fund Type: Government securities fund

- Investment Horizon: 4-7 years or more

- Risk Involved: Moderate

- Portfolio Focus: Long-term government bonds

- Ideal for: For investors seeking safe debt investment backed by government securities.

Bandhan GSF Investment

This debt fund usually invests in a diversified mix of government securities, corporate bonds, and money market instruments. It helps balance risk and returns.

Key Details:

- Fund Type: Diversified Debt fund

- Investment Horizon: Medium term

- Risk Involved: Moderate

- Portfolio Focus: Government and corporate bonds

- Ideal for: Investors seeking balanced fixed-income exposure.

Nippon India Nivesh Lakshya

Nippon India Nivesh Lakshya is a target-maturity debt fund that invests in high-quality bonds aligned with a specific maturity timeline. It aims to offer predictable returns if held until maturity.

Key Details:

- Fund Type: Target maturity debt fund

- Investment Horizon: Long term

- Risk Involved: Low to Moderate

- Portfolio Focus: High-rated bonds and government securities.

- Ideal for: For investors with a defined financial goal and fixed investment horizon.

Who Should Invest in and Avoid Debt Mutual Funds?

Debt Mutual Funds are ideal for investors looking for stable, low-risk returns, but may not be perfect for those aiming for high growth or aggressive wealth creation.

Who Should Invest in Debt Mutual Funds?

Debt mutual funds are ideal for:

- Conservative Investors

- Short-to-medium term goals

- Retirees or income-focused

- For portfolio diversification

- For savings accounts or fixed deposits

Who Should Avoid Debt Mutual Funds?

These investors should avoid Debt mutual funds:

- Investors looking for high long-term debt mutual fund returnsfor the future

- Expecting guaranteed or fixed returns

- For beginners who are not aware of credit and interest risk

Taxation on Debt Mutual Fund

For investment in Debt mutual funds, investors must have a thorough idea about taxation rules. Taxation rules for debt mutual funds vary largely based on the duration of unit holding:

Short Term Capital Gains (STCG)

Gains for the period up to three years are termed as short-term capital gains (STCG). These gains are usually added to taxable income and taxed according to the applicable income tax slab.

Long Term Capital Gains (LTCG)

Long-term capital gains tax applies if the period exceeds three years. LTCG is taxed at the rate of 20%, with the benefit of indexation.

Pro Tip: Estimate the possible tax income on your debt mutual funds by using Tax Calculator and invest accordingly.

How to Invest in Debt Mutual Funds on Mysiponline?

Investing in debt mutual funds with MySIPonline is a fast nd convenient process.Here are the simple steps to follow:

- Step 1: Create Your Account

Sign up on MySIPonline for free, fill in your profile details and finish the KYC verification process.

- Step 2: Activate Auto Debit

Now set up a debit mandate to enable automatic SIP payments from your bank account.

- Step 3: Choose a Suitable Fund

Go through the available debt mutual funds and choose one that suits your financial goals and risk performance.

- Step 4: Complete the Investment

Now add the selected fund to your cart, decide your SIP start date, and finalise the transaction.

- Step 5: Track Your Portfolio

Lastly, use the dashboard to review your investment performance, SIP status and transaction history anytime.

Other Categories of Mutual Funds

Frequently Asked Questions

Debt mutual funds in India aim to offer stable returns with lower risk than equities and invest in:

- Government bonds

- Corporate debt

- Treasury bills

Investors can choose the best debt mutual funds based on:

- Historical performance

- Investment horizon

- Credit qualit

Yes, debt funds are safer than equity funds, but are carried with credit, interest rate, a nd liquidity risks. So, opting for the high-quality government or corporate bonds increases safety.

Top debt mutual funds for 3-5 year target usually include medium-duration or corporate bond funds, giving you predictable returns with moderate interest rate risk.

The best performing debt mutual funds mainly include medium-duration, gilt and target maturity funds, delivering steady returns while balancing risk and liquidity.

Debt funds can generate income via interest from bonds and money market instruments, with the potential for capital gains, thus influencing overall debt fund return.

Yes, debt funds often offer better post- tax returns and liquidity other than fixed deposits, while maintaining moderate risk, making them a popular alternative.

Depending upon the types of debt mutual funds, returns can be distributed:

- Monthly

- Quartely

- Annual dividends

Related Blogs & Videos

The related news, technologies, and resources from our team.

-1.webp)

-

1511

1511 -

7 Min. Read

7 Min. Read

.webp)

-

9604

-

11 Min. Read

-

3569

-

3 Min. Read

You can select three funds for compare.

You can select three funds for compare.