A Concise Account on the India’s New Tax Policy – GST

The Goods and Services Tax or GST, is likely to be put in motion from 1st July 2017, and is expected to rehabilitate the Indian Tax System. Now, a change of such magnitude brings in a series of questions like:

- What is GST?

- How it attempts to remodel the existing tax regime?

- Was it indeed necessary to refurbish the tax policies at such a grand level?

We shall figure out all these queries as we think through the article candidly.

Describing GST

GST can be defined as an all-inclusive, multi-stage, end-point tax which is imposed on every instance of value addition. Being a comprehensive tax system, it will apply collectively to all goods and services except a few, which have been specifically excluded from the realm of GST. It will also eradicate the present indirect tax setup, however, ‘Direct Tax’ system like Income Tax will remain unaltered. Benefits of GST at a glance:

- Removal of cascading effect from the tax system

- Eradication of vague system of state-taxation and induction of a uniform tax rate

- Boost the economy by sidelining the infiltrations within the tax regime

Now, let’s further decipher the intricacies of the new tax program by dissecting it into a suite of illustrations.

Let’s begin with the word, ‘All-Inclusive’. GST is a blanket tax that will replace the current indirect taxes i.e., Excise Duty, VAT, CST and Service Tax. Hence, instead of tax being levied at different stages with different names, a uniform tax called GST will be imposed at every lap of value addition to the product and/or service.

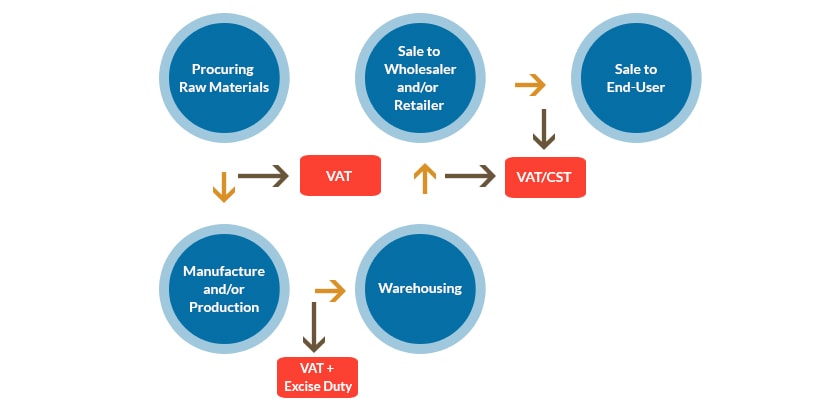

Multi-Stage: The term is self explanatory, which attempts to point out multifold levy of tax. There are several stages through which an article wafts, embarking from the purchase of raw materials and then, running through the production or manufacturing assembly. The product is then stored in a warehouse from where it lands up in the hands of the retailer, and thereafter, the final stage of the supply chain is executed, i.e., sale to the ultimate consumer.

Getting hold of the entire supply chain would come in real handy with the help of the following diagram:

Having discussed about the two attributes of GST, let’s now expound another pressing factor which is the rationale behind the new tax regime – End Point Levy. In the earlier tax system, Excise Duty was imposed on the manufactured/produced goods by the Central Government at the time of their removal - for sale, transfer to depot, captive consumption, and transfer to another place/unit and, even for fee distribution as samples. Further, VAT and CST was levied by the State Government in every subsequent case of intra-state and inter-state sales, respectively.

Thus, the primitive tax system would appear as follows:

How It Attempts to Remodel The Existing Tax Network?

The new tax system has been revised to work on an entirely different concept. In case of intra-state sales, the tax collected will have to be deposited to the credit of State and Central government in equal proportions, respectively. However, in the case of inter-state sales, the entire tax amount will be handed over to the Central government who will then disburse the tax to the State governments in the proportion it may deem appropriate. Let’s understand the new concept with the help of the following illustration:

Suppose, a product is manufactured in West Bengal and travels all the way down to Punjab for its final consumption. Now, GST being a destination-based levy will be received by the Punjab government, and West Bengal would lose the tax at the manufacturing and warehousing stages to the Punjab Government. Hence, the Punjab government will earn the tax on the point of final sale. Thus, there’s a complete makeover in the current tax system with the commencement of the new scheme.

Unfolding the Concept of Value-Addition

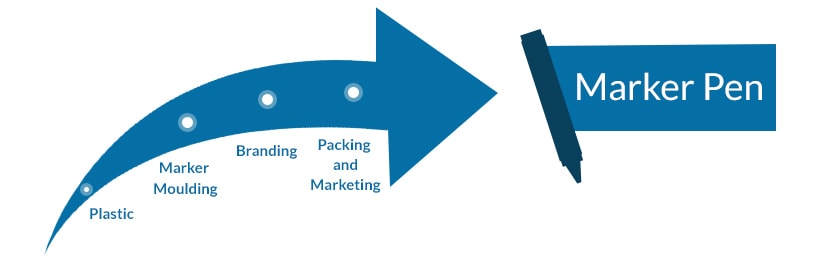

Now, in the entire write-up, a term has been constantly flashing-Value Addition. What is it? Let’s understand with an example.

Suppose a manufacturer desires to make a marker pen. The ingredient required is plastic. Once the plastic is molded into a marker barrel, its value gets energised. Moreover, the finished marker will be sold to the warehouse keeper where the process of branding will be executed to further enhance its value and then finally, value addition will be wrapped up at the stage of packaging and marketing outlay.

The Significance of GST

Having discussed the definition of GST in full, let’s now talk about the role it will play in rejuvenating the realm of Indian Taxation and thus, the Indian Economy.

In the present scenario, the Indian Taxation System operates on both sides of the coin - Direct Tax and Indirect Tax. While the direct tax liability has to be discharged in full by the assessee himself and there is no alternative to such disposal, the burden of Indirect Taxes can be transferred to the ultimate consumer who would be liable for paying not only the price of the commodity, but also the associated band of tax. This is because the retailer pays the tax to the credit of the government at the time of purchase of the commodity from the wholesaler, and for its recovery as well as the recovery of the amount to be paid to the government, the liability is shifted to the end user.

Goods and Services Tax is thus, implemented to synthesise such issues. It encompasses a system of Input Tax Credit which will enable the sellers to claim the tax they have already paid, which will reduce the final liability on the end consumer.